Stocks had another rough week. The S&P 500 flirted with the June lows and swung back into bear market territory. Investors are worried about inflation, the Fed, the economy, the Russia-Ukraine war, among other market challenges.

- The market is experiencing peak bearishness.

- This coincides with peak hawkishness from the Federal Reserve, as it projects more interest rate hikes.

- Fed Chair Jerome Powell warns that putting inflation behind us may not be painless.

- A down swing in inflation could prompt the Fed to pause.

One potential positive is overall market sentiment is getting quite pessimistic, in some cases reaching levels last seen in March 2020 and even March 2009. Both periods presented major buying opportunities. Various sentiment polls are flashing extreme pessimism, which from a contrarian point of view could be quite bullish. The reasoning is once all the bears have sold, there are only buyers left.

Considering October is known as a “bear market killer,” we continue to think major lows could be near. The stock market saw major lows in October in 1957, 1960, 1966, 1974, 1984, 1990, 1994, 1998, 2002, and 2011. In fact, no month has seen more major market lows than October. We wouldn’t be surprised if 2022 joined this list.

The Fed Wants to Get Inflation Behind Us, But There Isn’t a Painless Way to Do That

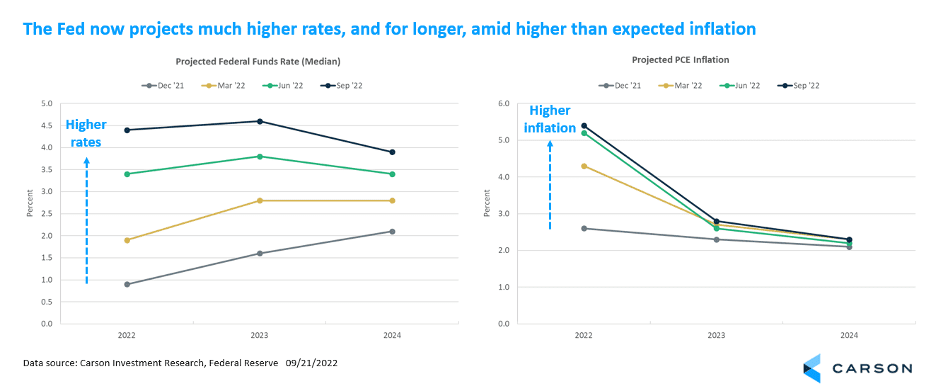

An aggressive Federal Reserve raised its target policy rate by another 0.75%, taking it to the 3.0-3.25% range. This was the fifth hike this year and third successive 0.75% rate hike by a Fed looking to get on top of inflation. While it was largely expected, the big surprise was how high the Fed projected the interest rate to rise over the next year. In short, there’s more tightening to come.

By the end of 2022, the Fed projects policy rates to reach 4.4%, a full percentage point above what was projected just three months ago in June. As of the end of 2023, the Fed now expects the target rate to hit 4.6%, about 0.8% above the previous projection. These projections have risen rapidly this year amid 40-year highs in inflation. Crucially, the Fed now projects staying at these high rates through 2024 at least.

The Fed is strongly committed to bringing inflation back down, and Fed members believe that is the key to sustaining a healthy economy and labor market over the long term. However, they also believe there is no painless way to do it, and that was a big takeaway from the meeting. It’s worth quoting Fed Chair Powell in full:

“We’re never going to say that there are too many people working, but the real point is that people are really suffering from inflation. If we want another period of a very strong labor market, we have got to get inflation behind us. I wish there were a painless way to do that. There isn’t.”

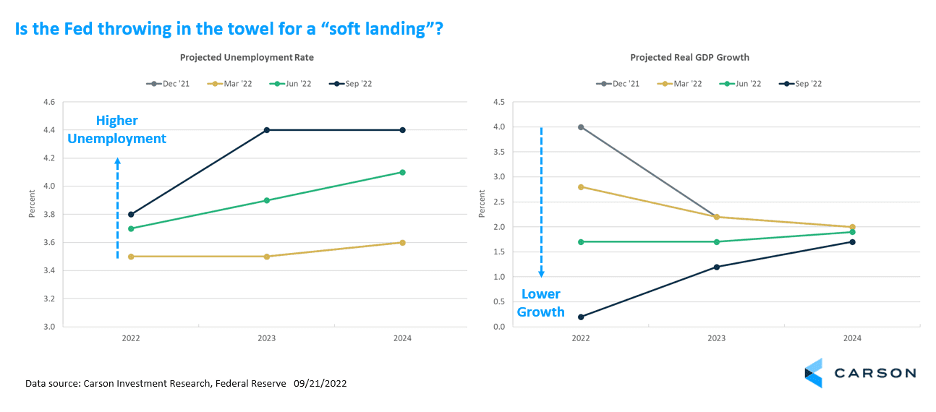

This came across in the Fed’s latest economic projections. It slashed estimates of 2022 GDP growth from 1.7% to 0.2%, and for 2023, from 1.7% to 1.2%. The Fed now expects unemployment to peak at 4.4% in 2023, up from the June projection of 3.9% (the rate is currently 3.7%). That translates to about 1.2 million more people losing their jobs.

Up until June, central bankers were clearly hoping to get away with small upticks in the unemployment rate, i.e., a “soft landing.” No longer. The latest projections basically amount to a recession, although perhaps, a mild one. The problem is once unemployment starts to rise, it’s not exactly easy to cap it at a particular number.

Are There Any Positives At All?

Powell did lay out a scenario for a soft landing. It’s a challenging path, but not implausible in our view.

- The labor market is currently imbalanced, with demand outrunning supply. But job vacancies (representing demand) are at such a high level that they could potentially fall without much of an increase in unemployment. However, this would be a big break from what we’ve seen in the past, as falling vacancies have typically been associated with more layoffs. Also, workers quit their jobs at a much higher rate after the pandemic (for better-paying jobs), but that’s slowing down now. If this continues, it should also ease the supply-demand imbalance and associated wage pressures.

- Inflation expectations, both amongst consumers and market participants, have been well anchored. That means there’s no expectations-related inflation spiral. This occurs when people expect higher prices in the future, so they buy now to get ahead of inflation and, in turn, drive up prices.

- The current inflation has been partly caused by a series of supply shocks, beginning with the pandemic and the economic reopening, and amplified by the Russia-Ukraine war. These weren’t present in prior business cycles. Of course, the Fed expected to see supply-side healing by now, but it hasn’t happened yet.

The upward shift in rate projections is likely to be a one-time adjustment that reflects the current high inflation levels, as opposed to the beginning of a series of upward shifts. Several leading indicators point to easing supply-chain pressures and lower prices. It’s just going to take a little more time to show up in official inflation numbers. Just as an example, the Producer Price Index indicates that margins for auto dealers are falling quickly, which means prices for used cars should follow in short order.

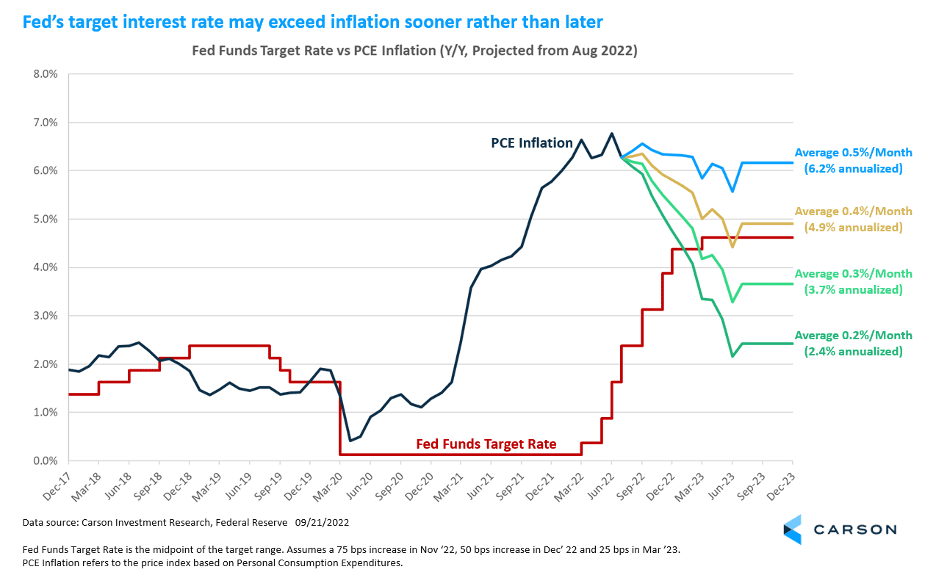

So, there is a high likelihood that the federal funds target rate (as projected) may rise above year-over-year inflation numbers within the first half of 2023. The chart below shows various projections for PCE inflation (the Fed’s preferred measure), based on average monthly price changes over the next 15 months. This assumes the Fed will raise rates by another 0.75% in November, 0.50% in December and 0.25% in March 2023. In our view, the scenario in which price increases average 0.3% month-over-month is quite plausible. That would take PCE inflation down to 3.7% by mid-2023.

Of course, this assumes there are no more shocks, such as the Russia-Ukraine war presented. That really is the key, as a convincing deceleration in prices is required for the Fed to pivot away from its current aggressive stance.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

Compliance Case #01497141