It is Thanksgiving week, so we want to review a few reasons for investors to be thankful. Yes, it has been a tough year. But things are looking better, and we expect more improvement in 2023.

Gridlock Can Be Good

The first reason to be thankful is stocks have continued to rally off their October lows, and now we have another potential positive: gridlock.

- Stocks continue to rally amid various concerns.

- Gridlock in Washington could be another positive for stocks.

- The U.S. consumer remains quite healthy — a reason to be thankful.

- More positive signs point to inflation peaking and rolling over.

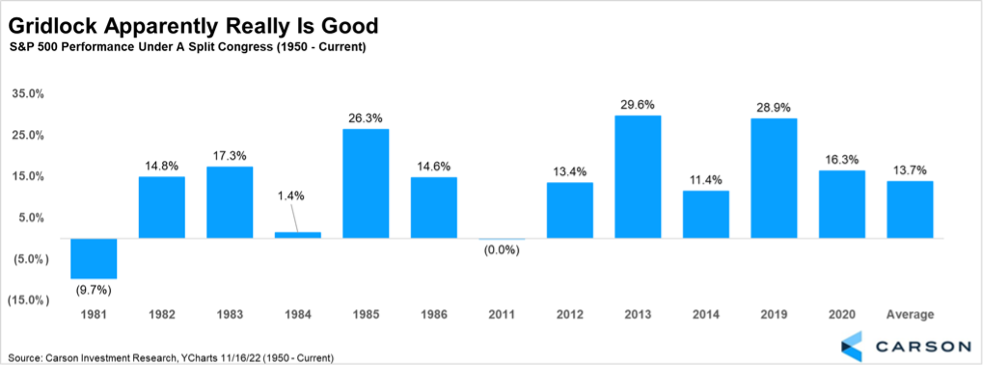

Midterm voting is over. While the official results aren’t quite in yet, we do know Congress will be split. As of now, Democrats hold 50 seats in the Senate, which means they will maintain control, while Republicans gained their 218th seat in the House, which means they will hold a slim majority. The bottom line is neither Democrats nor Republicans have large majorities in either chamber; in fact, they are both near historical lows.

There’s an old saying that ‘gridlock is good’ for the markets, as Washington can’t do much when no one can agree. The chart below shows the S&P 500’s performance during the years of divided government since 1950. The average return for stocks was a very solid 15.7%, with only 1981 falling significantly and 2011 breaking even. The other years saw solid returns, suggesting gridlock indeed could be positive for the markets.

Lastly, Republicans have a narrow majority in the House. At the time of this report, they are expected to have a three-seat majority, the narrowest margin their party has held since 2001 and 2002. We reviewed years with narrow margins and found they generally lead to larger gains. When the House majority is held by fewer than 20 seats, the S&P 500 has gained a median of 19.5% since World War II. Additionally, the first year of a new Congress with a narrow majority, which in this case would be 2023, has been higher nine of the past 10 times.

The U.S. Consumer Remains Strong

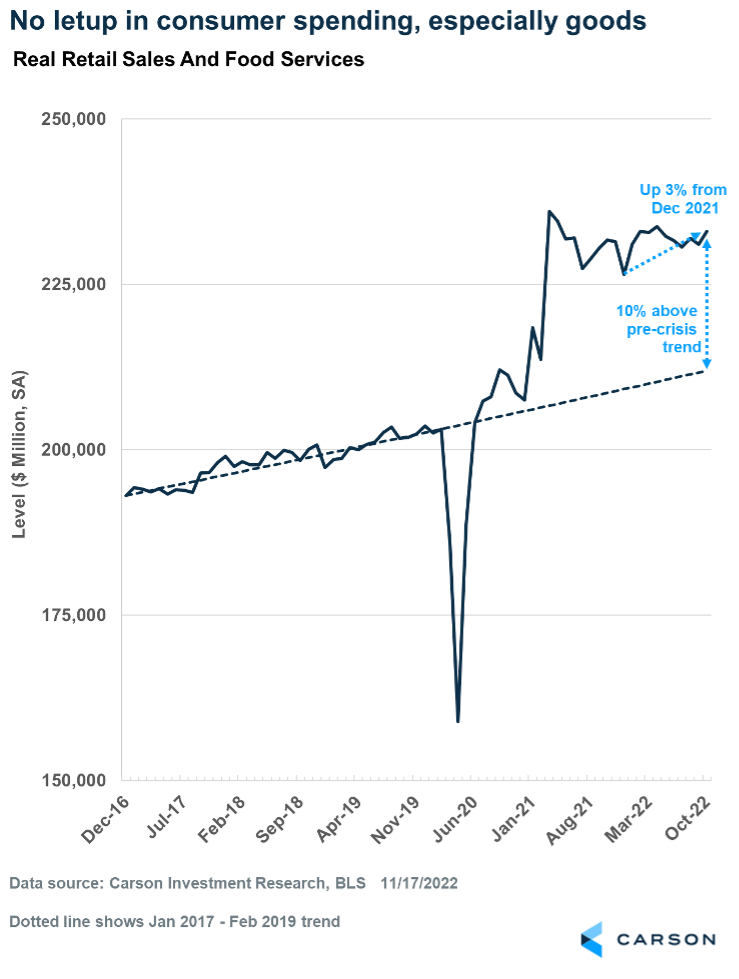

The next reason to be thankful is the consumer remains extremely strong. In fact, the consumer’s strength in the face of numerous obstacles is one of the biggest surprises of the year. Last week, October retail sales rose 1.3%, beating expectations for a 1% jump. Prior months were revised higher as well.

One significant reason was stronger gasoline sales, which was a function of prices at the pump rebounding. But sales were also strong across most other areas, including auto sales, restaurant and bar sales, online spending, and even building materials.

One way to account for higher prices across several of these categories is to look at “real retail sales,” i.e., sales adjusted for prices. Real sales rose 0.8% in October, which is the fastest pace in eight months. Real sales had slowed in the summer (May-August), but they are picking up again — a sign of rising “real” incomes thanks to a pullback in inflation. Real sales are now up 3% from December 2021 through October. And in real terms, consumers are spending 10% more than expected if we just extended the pre-pandemic trendline. That’s massive!

Since consumer spending makes up nearly 70% of the U.S. economy, real sales offer another clue that a recession is not right around the corner. Many have been sounding the alarm, but with a consumer this strong we don’t see a recession on the horizon. And that’s definitely something to be thankful for.

More Good News on Inflation

As we noted last week, inflation at the consumer level is coming down quicker than expected. Used cars, apparel, and medical insurance all saw solid improvements. Additionally, rent and food inflation are finally showing signs of slowing as well. These sectors were significant contributors to the massive inflation spike.

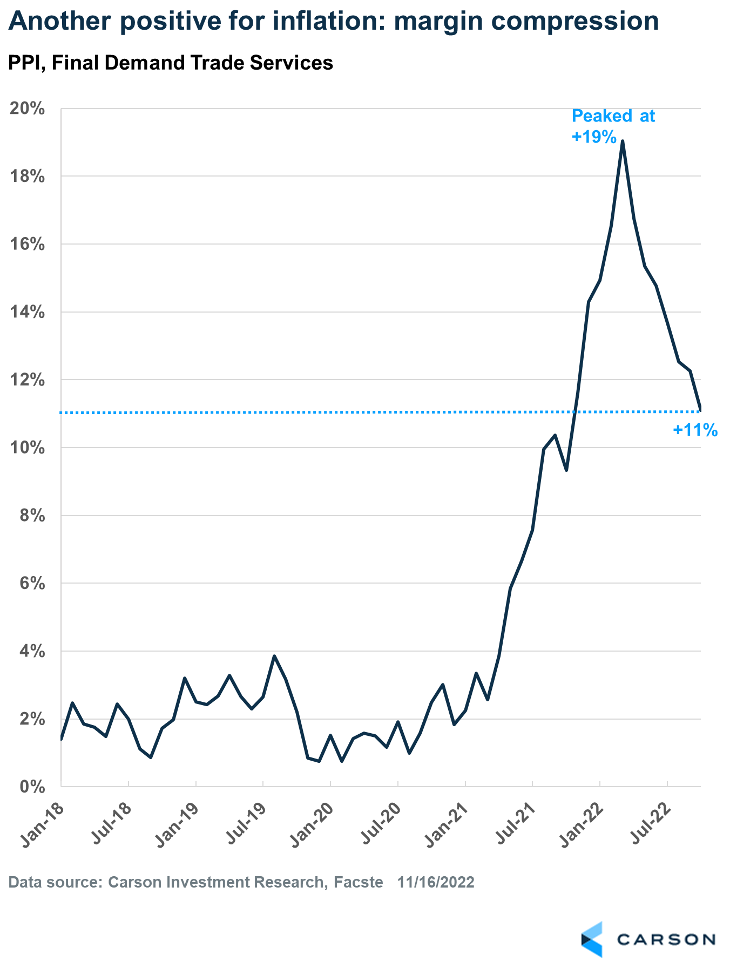

Last week also produced good news from inflation at the producer level. That’s positive for consumers, because if it costs less to produce goods, companies can sell them for lower prices. In fact, the Producer Price Index (PPI) in October fell 0.5% after falling significantly the last few months. The year-over-year pace is now about 11%, having decelerated from a peak of 19% in March 2022. It still has further to go to return to the pre-pandemic pace of about 2%, but the trend is very encouraging.

All of this means less pressure on the Fed to continue its extremely aggressive stance on hiking rates to slow inflation. The Fed has given the patient a lot of medicine, and with real signs of improvement Fed members might pause to let the medicine work its magic. In fact, we think the odds of the Fed pausing rate hikes early next year are increasing greatly.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

Ryan and Sonu Varghese are non-registered associates of Cetera Advisor Networks.

Crypto-Currencies, Digital Assets and other Block-Chain related technology (such as Bitcoin, Ethereum, NFTs and others) are not securities, not regulated, and not approved products offered by Cetera Advisor Networks LLC. Crypto-currencies and other block-chain related non-securities products cannot be recommended, offered, or held by the firm.

Compliance Case # 01559707